NGS Providers: Go-to Resources Clients and Key Customers for NGS Suppliers

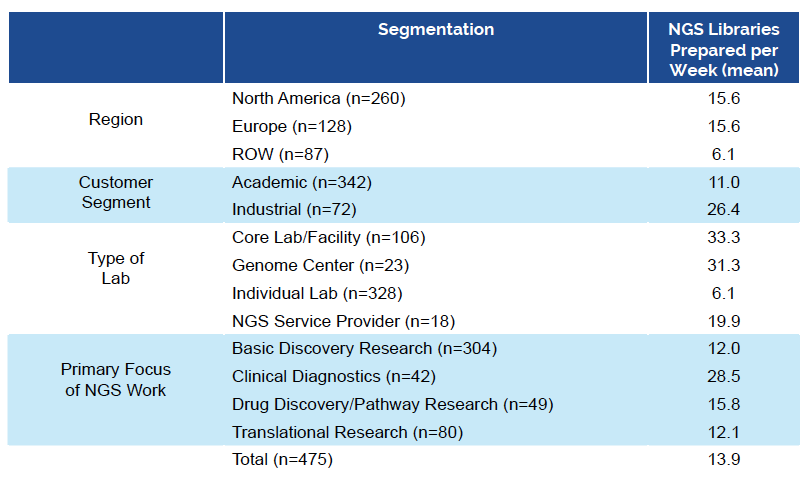

Providers of NGS services—broadly defined to include core labs/ facilities, genome centers and NGS service providers—are a dominant and influential customer in this market. In a recent NGS market study we conducted, one-third of our respondents identified themselves as working in a lab that provides NGS services. By our estimation, these labs prepare two-thirds of the NGS libraries.

NGS service providers conservatively prepare five times the number of NGS libraries per week as those prepared by individual labs (those labs that don’t routinely provide NGS as a service). NGS service providers not only prepare more libraries, but they also perform a wider range of NGS applications, start with a wider variety of biological samples and are more likely to have automated some phase of NGS library prep workflow.

To support this level of activity, NGS providers, especially core labs, tend to have bigger labs with higher headcount and larger annual budgets—not only for NGS operations in general, but also to support NGS library prep in particular.

Respondents who self-identified their lab as a core lab were more likely to work in the industrial for-profit customer segment. Likewise, those respondents who indicated that the primary focus of their lab’s NGS work is clinical diagnostics are also more likely to have identified their lab as a core lab as well.

For more information about this report, visit: Reports/