The Chromatography Market: Outlook to 2020

The chromatography market is projected to grow at rate of 3.7% during the next five years. By 2020, the chromatography market will reach almost $10 billion in sales. In our report, The Chromatography Market: Outlook to 2020, we examine both gas and liquid separation techniques.

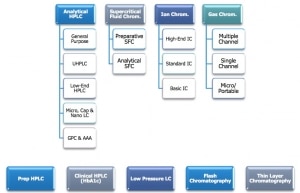

Chromatography is a versatile method of separating and analyzing the components or solutes within complex chemical mixtures and is widely used across multiple market segments. Using chromatography, separation is achieved by allowing a sample within a solvent to be carried by a mobile phase (in liquid or gaseous form) through an adsorbent (typically a column, gel, or paper) serving as a stationary phase, so that each individual compound within the mixture is adsorbed into a separate layer and therefore eluted at different times. The amount of separation achieved is based on the differential partitioning between the mobile and stationary phases. Our report examines 18 different product types, grouped into nine technology segments consisting of analytical and prep HPLC, clinical HPLC, GC, IC, SFC, LPLC, flash, and TLC. This report includes:

- Technology Overview

- Demand (Market Size) by Product

- Demand (Market Size) by Region

- Application Segmentation

- Competitive Situation & Market Share

Chromatography Market Structure

Analytical HPLC and GC collectively accounted for nearly three-quarters of total demand in the chromatography market. Clinical HPLC (HbA1c) is the fastest growing segment with an average rate of 8.7%. In contrast, the demand for thin-layer chromatography is declining resulting in a stagnant market for this technique. Within this report, each major technique is examined in terms of:

- Technology Overview

- Product Segmentation

- Unit Shipments

- Application Segmentation

- Regional Demand

- Competitive Situation

- Recent Developments

Pharmaceutical and life science research continues to drive demand for chromatography instruments and consumables on a global scale. However, the technique is increasingly important in the clinical, food and environmental testing market segments. The demands for innovative solutions in specific application areas have forced chromatography companies to broaden their technology portfolios either through mergers or collaborative agreements. At the same time these companies are being called upon to become more solution- and service-oriented.

Agilent and Waters are dominant players in the overall chromatography market with strong positions in both the GC and HPLC segments. Thermo Fisher Scientific has a strong presence in all segments and an especially strong position in ion chromatography. The combined strength of MilliporeSigma will see the company making strides to win share especially in consumables. Other vendors compete with more focus, for example: GE Healthcare in the preparative HPLC and LPLC segments and Bio-Rad in the rapidly growing clinical HPLC segment..

PerkinElmer and Phenomenex are in the top 10 of all vendors and other important suppliers include Shimadzu, TOSOH, VWR, and Hitachi. Numerous companies make up the remainder of the highly competitive chromatography market, typically by capturing specialized niches in the aftermarket sales.

Given the broad range of applications for chromatography, we expect to see increasing demand for more specialized instruments, more sensitive detection and enhanced data integration.

Companies Mentioned In This Report:

Agilent

Avantor

Bio-Rad

Biotage

GE Healthcare

GL Sciences

Grace

Hitachi

Honeywell

Industrial gas suppliers

Jasco

Merck

Metrohm

PerkinElmer

Phenomenex

Restek

SCIEX (Danaher)

Shimadzu

Showa Denko

Sigma-Aldrich (Merck)

Techcomp

Thermo Fisher

TOSOH

VWR

Waters

YMC