NGS Informatics – Competing in a Converging Market

The 2017 Market for NGS Informatics: Probing the Commercial Landscape is designed to help companies navigate the crowded market for products and services that support Next Generation Sequencing (NGS) data analysis and storage.

Scientists face many challenges when choosing a solution: it is often difficult to determine the significance of results, the storage space needed for their data is astronomical, there are too many choices, and many current solutions lack desired features. All of these factors create uncertainty over which solution is right for them.

Our report brings the important perspective of end-users in labs that employ NGS to the discussions currently taking place among marketing and product development teams trying to differentiate their solutions amidst the hype that surrounds this segment of the market.

In planning our research, we set out to explore the following critical issues:

1) Understand the market for NGS bioinformatics solution providers across the following attributes:

- Pricing structure

- Product mix

- Branding

- Participation areas (identifying high potential vs. mature segments/components)

- Business models

2) Identify areas ripe for new product development, based on customer needs/wants.

3) Understand the unique challenges and opportunities in clinical NGS diagnostics:

- Adoption rate of NGS analytics in clinical environments.

- End-user (clinicians, decision-makers) perspectives on NGS analytics products.

4) Explore customer concerns with data handling, storage, privacy, and security.

It was not a surprise to us that Illumina and Thermo Fisher sequencing instruments are by far the most-used NGS platforms, while other market players such as Pacific Bioscience and Oxford Nanopore are gradually capturing more market share. Despite now being discontinued, Roche’s 454 GS series is still used by 11% of the scientists responding to our survey.

Four hundred end-users of NGS informatics solutions in North America, Europe, and Asia Pacific participated in this study. Respondents were from various laboratory types including basic research, translational research, clinical diagnostics, pharmaceutical R&D, and core labs, with over half from translational research and clinical diagnostics laboratories.

Again, we expected that there would be a strong correlation between the leading instrument and awareness of their accompanying informatics packages. Illumina’s BaseSpace solutions, QIAGEN’s CLC Genomics Workbench and Ingenuity Variant/Pathway Analysis solutions, and Thermo Fisher’s Ion Reporter have the highest levels of awareness as well as usage among the respondents. What was most surprising is that the majority of commercially available sources of NGS data analysis solutions are “invisible” to end-users—they are almost completely unaware of their availability. This isn’t just a marketing challenge for theses software vendors (although stronger marketing is clearly needed). In the absence of developing the “killer app” that overcomes the bottlenecks discussed in our report, smaller vendors must forge alliances with the instrument vendors.

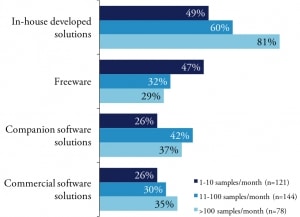

The five market segments we studied vary in how they obtain the software used for analysis and integration of their NGS data. Regardless, all scientists rely on a mix of internally developed software, freeware distributed throughout the scientific community, commercial packages from small independent vendors, software embedded in analytical instruments and proprietary software designed to run on enterprise solutions. The heterogeneity of the software environment—particularly at large research organizations—reflects the rapid evolution of NGS and the difficulty of integrating not only disparate data but also multiple application tools. Scientists engaged in basic research are more likely to use freeware whereas pharma/biotech scientists are more likely than their academic counterparts to use software developed in-house.

The common use of free and in-house NGS software in addition to that embedded with instruments would suggest a robust market for third-party commercial software vendors. Software from commercial developers is usually designed to be more reliable and offer greater support than freeware, and is often more economical than customized in-house development. Scientists who use freeware or in-house software to analyze and integrate their genomics data would be influenced to switch to commercial software if it was demonstrated to have greater capabilities and features. In our past work we have found that scientists’ software decisions are not driven by concerns about installation, documentation or future upgrades and enhancements. They are challenged by an inability to find exactly what they need in a commercial software package. NGS user requirements for software are often unique from customer to customer, making it difficult for commercial software vendors to create universal out-of-box solutions. In order to meet customer needs, out-of-box solutions need to include post sales support that permits customization by the vendor or by the end-user. Alternatively, commercial software vendors could market complete customization solutions for larger companies or institutions.

The NGS market is one characterized by convergence — an accelerated blurring of distinctions between previously well-defined scientific disciplines, between biology and computing, and even between competitors. Spurred by the declining cost of sequencing, the pace of convergence is likely to only quicken. But the results of this survey also indicate that, for the majority of genomic researchers, the collection and analysis of NGS data is a means to an end, and but one step in an ongoing experimental process.

Many, not all, researchers using NGS are generating new data in their experiments—not working in silico using data previously collected. The conventional wisdom is that scientists are “overwhelmed” by NGS data may be misstating the problem. In fact, it is more likely that many scientists working with NGS are simply not taking full advantage of the data available, and are instead generating the data within the context of the experiment at hand simply because they can. We see this in our survey data based on levels of throughput. Lower throughput users report experiencing more problems and bottlenecks than high throughput labs.

Software Used by Throughput (excerpt from our report)

This presents commercial vendors with the challenge of marketing advanced solutions to the high throughput segment of the NGS market, while simultaneously educating mainstream researchers as to the possibilities that become more attainable by taking advantage of advanced informatics solutions. In other words, where the purpose of traditional marketing is usually to focus product positioning and develop targeted communications, the NGS informatics market demands that vendors identify unarticulated customer needs that represent the opportunities made possible by the convergence of biology and computing. Success in the NGS market will be derived from an ability to foresee the trajectory of future improvements that will result from convergence, and the scientific and economic consequences of those improvements.

Please download an Executive Summary and detailed Table of Contents. The 2017 Market for NGS Informatics: Probing the Commercial Landscape provides deep insights into the needs of end-users so that solutions to the many challenges faced by NGS labs can be overcome.